Quantitative engine for risk analysis and management for trading

Risk Management System helps traders evaluate the risk of any trading instrument in with informed decision making with several risk parameters such as option greeks thru an advanced quantitative calculations, comprehensive market data processing, and actionable risk indicators. The system enables effective risk assessment in dynamic markets.

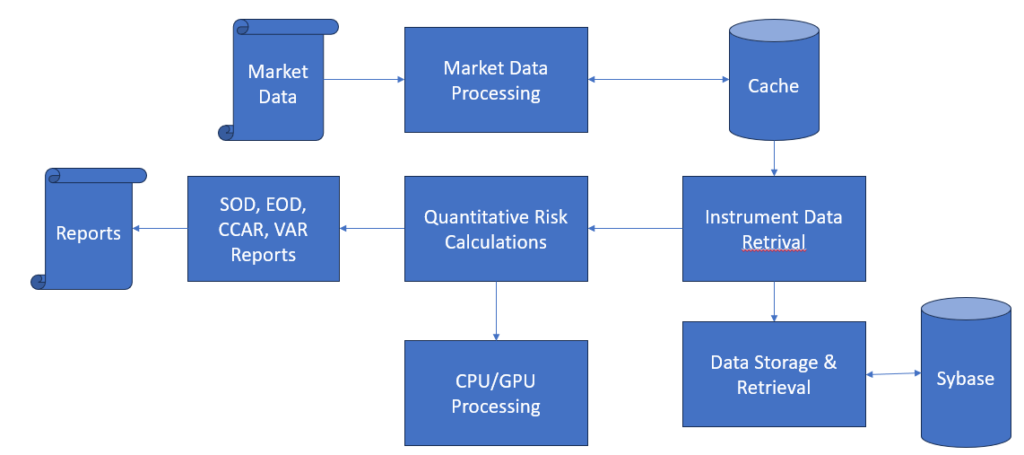

Implementation Process

Market Data Processing

Collects and processes real-time market data from trusted sources, including price feeds, volume, and volatility, ensuring that the system works with accurate and up-to-date data.

Cache & Database Management

Stores processed market data, trading positions, and calculated metrics in high-performance caches and persistent databases for fast retrieval, historical analysis, and reporting.

Quantitative Engine

Calculates options Greeks (Delta, Gamma, Theta, Vega, Rho) and other key metrics to measure the sensitivity of instruments to market movements. Provides position tracking to monitor exposure and risk at the instrument levels.

Daily Reports

The system enables traders with daily start of day, end of day reports and customized reports configured for trader needs for set of instruments configured. The reposts consists risk exposure, instrument performance, and market.

Instrument Positioning

The system also integrates with high performance instrument positioning system that updates information about most recent instrument positioning in the risk management system.

Market Risk Analysis

Several market instruments that are prone to high volatility are configured for frequent analysis such as CCAR, VAR to ensure risks are managed and mitigated.

Technical Stack

- Java, Java EE

- Gemfire & Sybase